A time where we reminiscent and reflect on the the things we regret doing or not doing, what we have achieved, and most importantly the lessons learnt for the past year.

This year was a year where I experienced the loss of a loved one, met and fell in love with a wonderful girl, spent time rekindling old friendships and quality family time, picked up a new language, travelled overseas to see wonderful sights of nature, "gave birth" to my blog, and read many wonderful books contributing to my personal and spiritual growth.

Looking at the myself now, I feel more accomplished, fulfilled intrinsically than I was one year ago.

No major regrets this year was an additional sweetener. :-)

Looking forward in 2013, I strive to grow to become a more balanced person, while embracing life during this process.

Like what the late Zig Ziglar said before: " Be grateful of what you have, while in pursuit of what you want."

Wishing everybody a Happy and Prosperous 2013! Cheers!

Now for my stock commentary--->

Portfolio Commentary

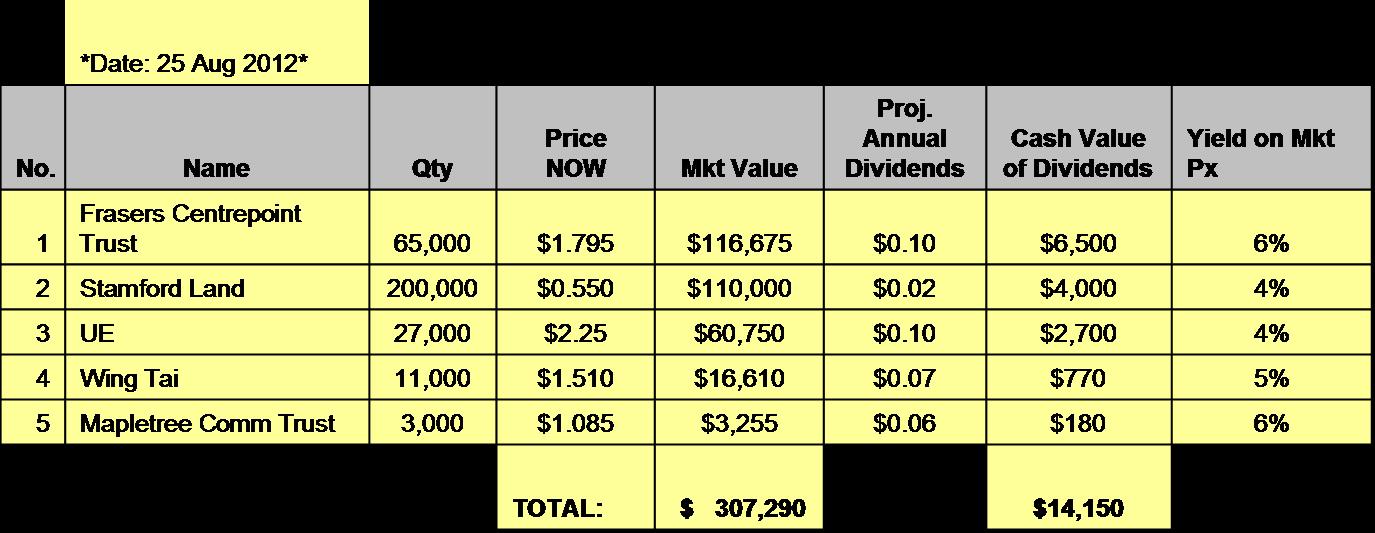

Portfolio @ start of the year:

Portfolio @ end of the year:

2012 saw the largest increase in my portfolio size in a single year since the year i started buying stocks.

The total market value of my stocks increased from $260k to $384k.

This represents a paper gain of $124k. Very tempted to take profits!

Albeit being paper profits, the performance was way beyond my expectations and I am happy that the hours/hard work I spent doing my qualitative & quantitative analysis paid off, plus alot of help from Mr Market, of course!

The amazing thing was this gain was primarily due to price appreciation and the reinvestment of dividends, as no leverage was used, and only a little savings was deployed (I injected only $10k additional capital from my cash holdings this year).

Nonetheless, stock prices are not as important as the value of the business behind the stock. I will be reassessing each company in my portfolio again on their own merits and decide in due course if there is a need for taking of some profits to recycle capital. Like what Peter Lynch said in his classic One Up On Wall Street, "Check the story periodically".

An intangible improvement in the quality and sustainability my portfolio also occurred this year, as I reduced my exposure in Australian Hospitality and suburban malls to diversify into businesses that does Engineering, Singapore Hospitality, Commercial Ppty, Property Development, Retail. It can be quite thrilling to know that you have a stake in businesses you can visually see.

Miscellaneous thoughts --->

A key concept I came across this year was the analogy of approaching stock investment as a business analyst.

It is a very apt concept and analogy that helps us simplify our thoughts in this chaotic financial world of ours. I find it a very good way to approach my future investments, as a Business Analyst.

I stumbled upon this in articles written in a couple of blogs that I follow regularly, namely Drizzt of Investment Moats (http://www.investmentmoats.com/) and Mr B of 3Fs(http://foreverfinancialfreedom.blogspot.sg/).

Since I discovered the world of blogging, other blogs I follow regularly and gained immense knowledge and opinions from are ASSI for investment philosophies and thought processes (http://singaporeanstocksinvestor.blogspot.sg/),

Dividend Warrior, for his drive towards regular passive income (http://dividendsrichwarrior.blogspot.sg/), Singapore Man of Leisure for his fantastic outlook on life (http://singaporemanofleisure.blogspot.sg/), just to name a few.

These are very good investment blogs with quality posts on Value Investing which I learnt alot from as well. Thanks guys for sharing snippets of your lives and well written articles! Keep it up!

Readers might like to follow these good blogs.

I aim to continue on Part 4 Investment Philosophies thread with a writeup to share my views on a company's management. Stay tuned!

:-)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}